By James Pethokoukis

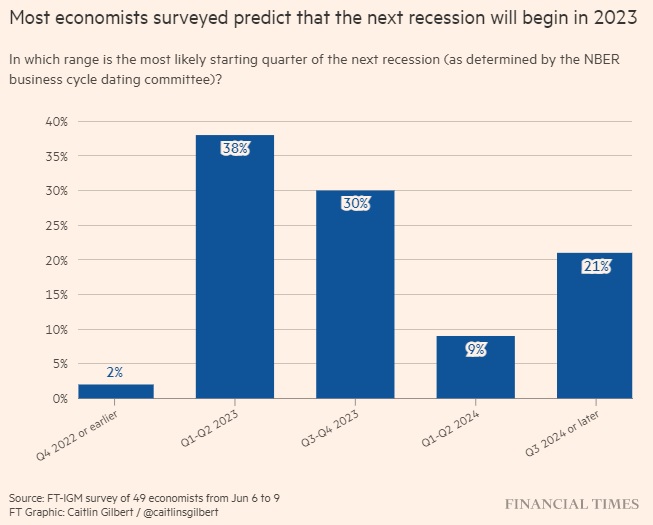

Look out below. An unsettling seven out of 10 economists—well, 70 percent of the ones polled by the Financial Times—think the US economy will suffer a recession next year. Of that gloomy group, 40 percent think a downturn will start in the first of half of 2023, with a third expecting one in the second half.

An important point: The poll specifies that the National Bureau of Economic Research will be the recession arbiter. That means consecutive negative quarters aren’t the definition of “recession” here. Rather, the NBER looks for a “significant decline in economic activity that is spread across the economy and lasts more than a few months.” We should hope the decline is so brief and so modest that it’s a tough call for the NBER. The eight-month contraction back in 2001 is an “official” NBER recession even though no two consecutive quarters were negative.

The survey results were collected between June 6 and June 9, and it’s likely that nothing has happened since then to make this group more optimistic. The May CPI report, out June 10, was hotter than expected, raising the prospect of faster-than-expected monetary tightening by the Federal Reserve. This from JPMorgan on Monday:

Two developments since the May CPI report reinforce the case for a more hawkish FOMC meeting on Wednesday, in our view. First, the startling rise in the longer-term inflation expectations in the University of Michigan’s consumer sentiment survey could imply a higher level of the nominal neutral interest rate. Second, according to the WSJ this afternoon, the Committee will not go into tomorrow’s two-day meeting constrained by their previous guidance that a 50bp meeting “would likely be appropriate.” As such, we now look for a 75bp hike on Wednesday. To the extent today’s report about Fed officials considering “surprising markets with a larger-than-expected 0.75pp interest rate increase” helps reinforce expectations for such a move, one might wonder whether the true surprise would actually be hiking 100bp, something we think is a non-trivial risk. After this week we look for two more 50bp hikes in July and September before the Committee slows to a 25bp hike per-meeting pace until reaching terminal funds at 3.25-3.50% early next year.

And, we now know, a 75bps hike is what we got yesterday from the Fed. None of this is helping anyone feel better about the Fed pulling off a soft landing—a scenario where the economy continues to grow but inflation cools off to the central bank’s comfort level. To turn to 2024 politics for a moment, Democrats should probably prefer a recession—if there’s going to be one—happening next year rather than in 2024. They’re going to want a strong rebound heading into the presidential election that November. (All this assumes the historical economy-election relationship is still valid.) This from Bloomberg, with another recession forecast:

Soaring prices are hurting Americans. The cure is going to hurt, too. It may take a recession to stamp out inflation — and it’s likely to happen on President Joe Biden’s watch. A downturn by the start of 2024, barely even on the radar just a few months ago, is now close to a three-in-four probability, according to the latest estimates by Bloomberg Economics. . . . [The] mood has turned sour at an alarming pace — putting Biden at risk of joining an unenvied club. From Jimmy Carter to George H.W. Bush to Donald Trump, one-term US presidents of the past half-century all had their re-election hopes fatally injured by the lingering effects of a recession.

Politics aside, no recession is obviously better. We should want long expansions that grind down unemployment and raise labor force participation to sustainable levels, at least as judged by the Fed. And the health of the current expansion is, unfortunately, in grave doubt.

The post Recession Odds Rising appeared first on American Enterprise Institute – AEI.