Conservative scholars and policymakers have given the Child Tax Credit (CTC) a lot of attention recently as an avenue to send families additional support while addressing declining fertility in the US. Expanding the CTC may seem attractive as a pro-family policy, but increasing its refundability, as recent proposals suggest, would increase work disincentives for low-income households. Policymakers should consider the pro-natal vs. pro-work tradeoff carefully, because weakening work incentives would risk returning to unsuccessful welfare policies and higher poverty rates.

One problem with current proposals to expand the CTC rests

with their increase to the refundability

aspect. Making a tax credit “refundable” means families who do not owe any

federal income taxes will still receive a check from the government for the

value of the tax credit. Currently, the refundable portion kicks in at $3,000

of earnings and gradually increases with earnings to a maximum of $1,400 per

child. Only families who owe taxes can claim the full $2,000-per-child CTC. It

is important to note that low-income families also receive the Earned Income Tax

Credit (EITC), a wage-supplement that rises more quickly with increased

earnings and offers a strong incentive to employment.

Last year, Senators Michael Bennet (D-CO) and Mitt Romney

(R-UT) proposed a CTC expansion that would increase the value of the CTC for

families with young children (age 0–5) and its refundability. Under the

Romney-Bennet proposal, families would receive a fully refundable $1,500 per

young child (age 0–5). Depending on their earnings and tax liability, they

could receive another $1,000 per child. For older children, families would

receive a fully refundable $1,000 per child, increasing to $2,000 per child

depending on earnings and tax liability. Additionally, the House passed the

HEROES Act earlier this year in response to the pandemic, which would expand

the CTC to a fully refundable $3,600

for young children (age 0–5) and $3,000 for older children, regardless of

earnings or tax liability. The Biden campaign has proposed the same CTC

expansion, proposing a monthly or quarterly distribution.

Benefit programs for low-income families already offer a mix of employment incentives and disincentives. For example, research shows the Supplemental Nutrition Assistance Program (SNAP) reduces employment, while the EITC increases employment. Many low-income families receive both SNAP and the EITC, making it necessary to consider how these programs interact, along with proposed expansions to the CTC.

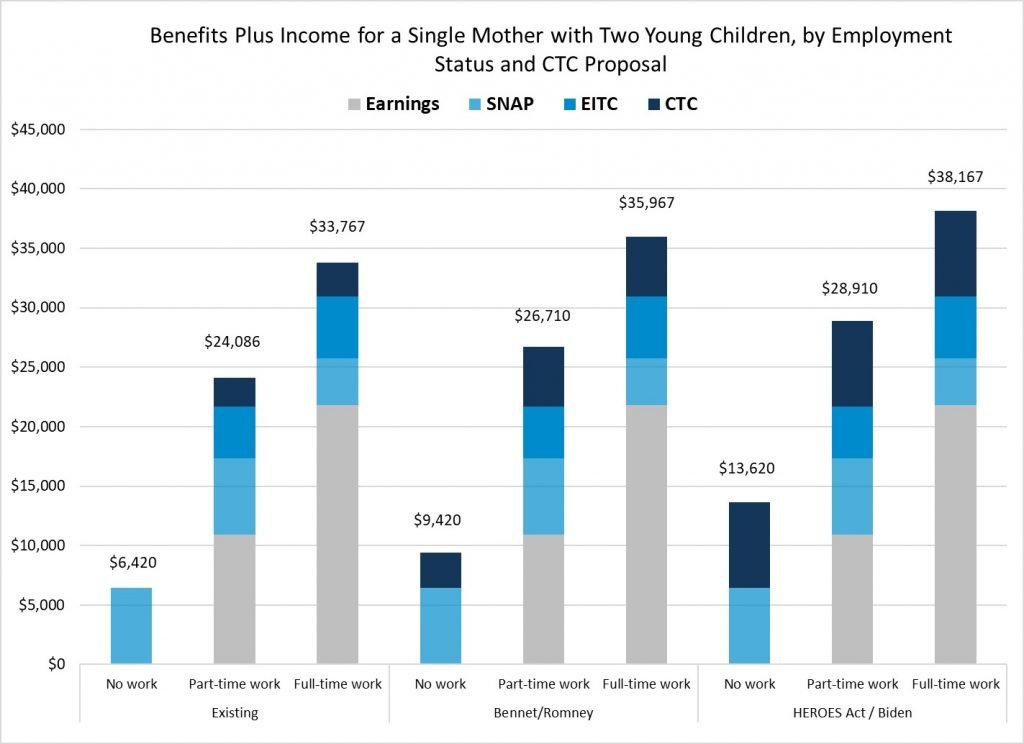

The figure below shows the total benefits a single mother with two young children would receive between the EITC, CTC, and SNAP depending on her earnings and the CTC proposal in place. The chart considers a mother who is not working, working part-time at $12 per hour ($10,920 in annual earnings), and working full-time at $12 per hour ($21,840 in annual earnings).

Even under the existing system, low-income families receive substantial government benefits to supplement their earnings. The CTC proposals would increase these benefits while also changing work incentives. The table below shows the “effective marginal tax rate” under each scenario outlined above, which reflects the percentage of each dollar of additional earnings compounded by benefits. Typically, effective marginal tax rates reflect the amount of additional earnings lost due to taxes and benefit reductions, but low-income families usually receive more than they pay in taxes because of the EITC and CTC. For simplicity, the positive percentage in the table below reflects the “bonus” families receive at different earnings levels, rather than showing lost income.

Under the existing system, a mother with two young children who moves from no work to part-time work will see $1.62 for every additional dollar earned, and $1.25 for each additional dollar earned if she starts working full-time. Under both CTC expansions, this hypothetical mother faces weaker work incentives. While the effects may seem small, they raise important questions about trading a larger CTC for a weaker pro-work policy.

This trade-off is avoidable. One alternative is to support expanding the CTC for families who owe federal income taxes, but expanding the EITC for low-income families to further increase work incentives. The table below reflects the “work bonus” by keeping the current CTC for low-income families but increasing the EITC by 50 percent instead. However, even an expanded EITC such as this raises concerns over marriage disincentives and the wisdom of using lump sum tax credits to boost incomes at the bottom.

Policy trade-offs almost always exist, but sacrificing pro-work policies for pro-natal ones risks returning to failed safety-net policies of the past, when idleness was rewarded and work was discouraged.

The post Pro-natal and pro-work conservatism appeared first on American Enterprise Institute – AEI.