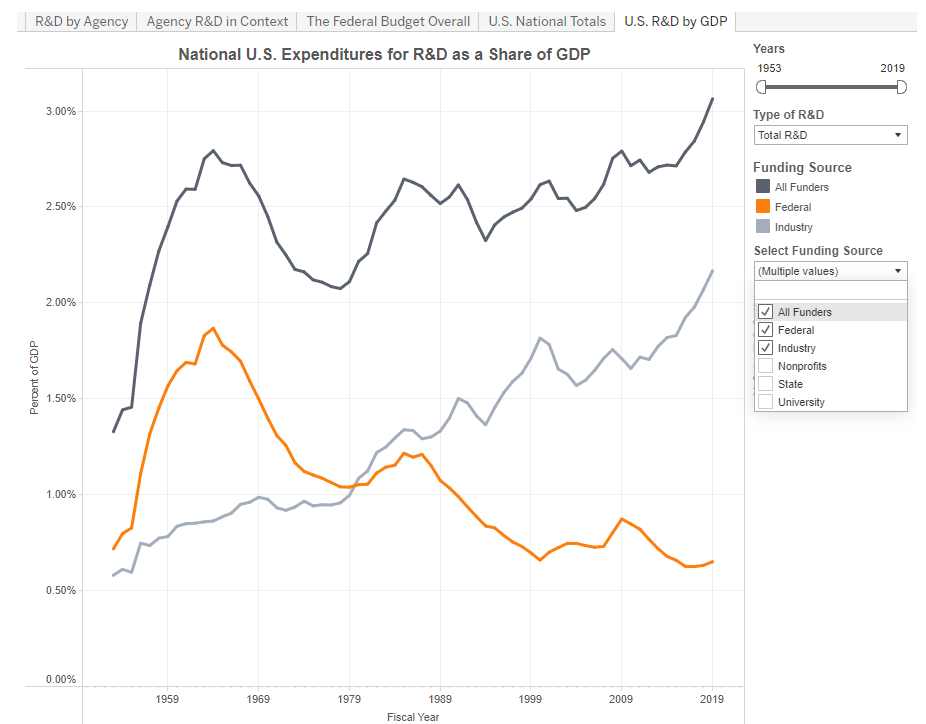

During the 1960s Space Race, the US spent nearly three percent of GDP on R&D, with two percent coming from Washington via the American taxpayer and one percent from business. Today, R&D is just over three percent, but the shares have flipped: two percent from business and one percent from government.

While nothing is truly free, my friends, investing in the American system of science and tech innovation offers a remarkable return on investment. It’s almost like a miracle machine that turns, say, $1 of investment into $5 worth of improved living standards, health, and productivity. Economist Benjamin F. Jones estimates that doubling both business and government R&D could raise US productivity and per-capita income growth by 0.5 percentage points annually.

I’m in favor of sharply boosting federal R&D spending. I think a return to Space Race levels is a good goal, especially when combined with reforms to get more bang for our taxpayer-funded investment buck.

Public policy could also do more to create a more encouraging environment for business investment, especially on the tax side and especially with upcoming tax expirations from the 2017 Tax Cuts and Jobs Act. In a new Tax Foundation report, “Leveraging Tax Policy to Bolster US Economic Growth Amid Competition with China,” Alex Muresianu, Alex Durante, and Erica York explain how bad tax policy hurts business investment:

If the tax code penalizes investment on the margin (by, for instance, not allowing companies to fully deduct their costs), companies will forgo marginal investments. In some cases, that might mean whole projects cease to become viable—a new factory, distribution center, power plant, or office park not worth the return on investment. In other cases, there might be slight enhancements to production: investing in a few additional trucks or machines to handle an increase in demand might be viable if the costs are fully deductible, but not if only 80 percent of the costs are.

The suggested reforms: Restore previous expensing rules (the immediate full deduction of investment costs in the year incurred) for R&D, machinery, and equipment; extend better cost recovery (allowing businesses to deduct investment costs more quickly) to structures investment; and avoid raising the corporate tax rate.

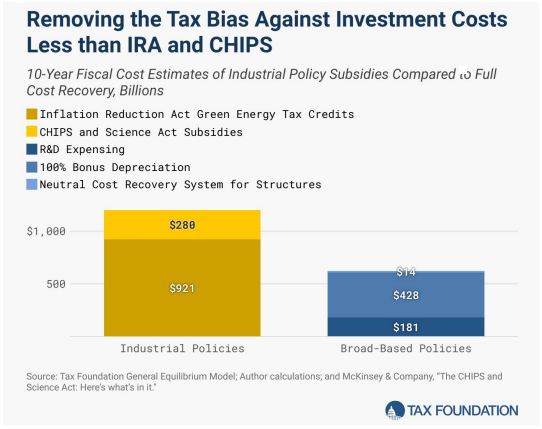

And the potential impact: “We estimate better cost recovery could boost US economic output by 1.7 percent and the size of the capital stock by 3.3 percent, at about half the budgetary cost of the Inflation Reduction Act’s green energy tax credits and the CHIPS and Science Act’s tax credits, grants, and spending authorizations.”

Keep in mind that under the current system, as of 2022, businesses must deduct R&D costs over five years, 15 years for foreign R&D. (A group of AEI scholars also recently proposed the immediate expensing of these costs, as was the law prior to the TCJA.) Additionally, the Tax Foundation paper presents better tax treatment of R&D as a key part of improving the US tax system’s competitiveness compared to China’s more generous R&D tax treatment.

From the report’s conclusion:

Rather than competing with China on the shifting sands of industrial policy, it is better to establish broad-based rules and incentives that lead to higher levels of investment, innovation, productivity, and economic growth over the long run. Tax law is only one policy area, but it is an important one, with strong evidence pointing to the effectiveness of better deductibility of capital costs in driving investment and productivity. China currently provides more favorable tax treatment for investment broadly, including better cost recovery for capital investment as well as many special tax breaks layered on top of that system aimed at specific industries. As Congress and the next president consider upcoming tax expirations from the 2017 tax law, they ought to prioritize reforming the tax code to make the United States more, not less, friendly to investment, which would be best accomplished through permanent, full cost recovery for all capital expenditures.

Policymakers should certainly consider how the tax code can better encourage business investment going forward. More federal R&D is necessary but not sufficient.

The post More American R&D Doesn’t Just Mean More US Government R&D appeared first on American Enterprise Institute – AEI.