Are we entering a new Space Age and a new Atomic Age? Maybe so, based on the huge drop in rocket-launch costs and renewed global interest in nuclear power. It sure would be awesome to live in a space-faring society able to generate vast amounts of abundant clean energy. The dreams of the immediate post-war decades would finally be fulfilled.

But those dreams also included high hopes for economic growth, including the expectation that the post-war boom in productivity and GDP growth would continue—or even accelerate. Alas, just as the Atomic Age and Space Age ended in the 1970s, so did those hopes for a forever boom.

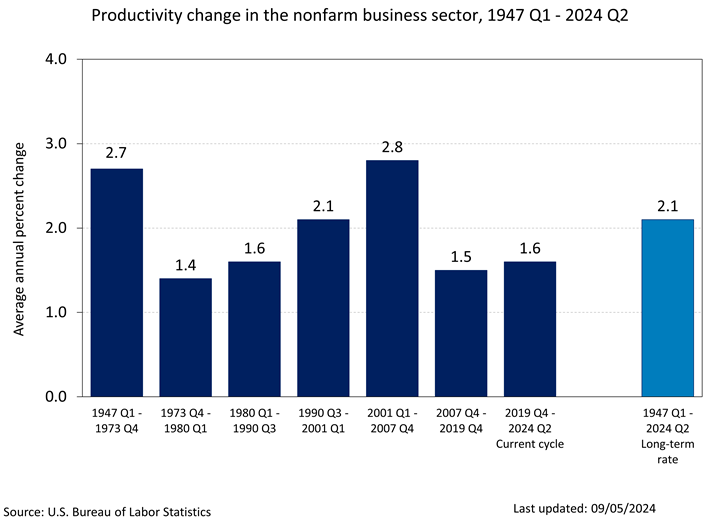

The early 1970s marked the end of a golden age of rapid technological progress and economic growth. From 1948 to 1973, the US economy grew four percent annually, with living standards nearly doubling. Labor productivity soared at three percent yearly, driven by human capital, physical capital, and, crucially, innovation. Then came the “Great Downshift” in 1973, as I term the surprising slowdown in my 2023 book, The Conservative Futurist: How To Create the Sci-Fi World We Were Promised, as productivity growth halved. Today’s economic consensus predicts future growth at just two percent annually, down from the overall postwar three percent, due to weak productivity growth and demographic headwinds.

But maybe along with a new Atomic Age and Space, we’ll also get a new age of rapid productivity growth. Earlier this month, the Bureau of Labor Statistics reported a 2.5 percent increase in nonfarm business sector labor productivity for Q2 2024, up from last month’s 2.3 percent estimate. Year-over-year, productivity rose 2.7 percent. Recent quarters show robust growth, likely due to post-pandemic efficiencies like worker reallocation, rather than AI. For this trend to persist, AI will likely need to take center stage. Prospects remain promising.

One productivity bull is longtime investment strategist Edward Yardeni, who recently offered several intriguing insights on the subject in a research note. Among them:

- First, recent productivity revisions challenge the “hard-landing” narrative, suggesting stronger economic performance than previously thought.

- Second, rising productivity growth has led to a significant decline in unit labor cost inflation, reaching its lowest rate since 2013 and indicating reduced underlying inflation pressures. (“This series is the best metric for underlying inflation pressures.”)

- Third, post-pandemic productivity growth has been primarily driven by capital intensity, particularly in tech sectors, with non-tech companies poised to benefit from AI going forward. (“As non-tech companies start to use artificial intelligence (AI), robotics, and automation better to address the skilled-labor gap, that will boost total factor productivity (e.g., how well labor composition and capital intensity are used by companies in producing goods and now services.”)

- Fourth, entrepreneurship has surged post-pandemic, with new business formations maintaining a significantly higher pace compared to pre-pandemic levels, including an increase in businesses likely to generate employment. (“Monthly new business formation has slowed this year but continues to run at a pace of 420,000 applications per month. That’s up from around 300,000 before the pandemic.”)

- Fifth, higher productivity growth supports Yaredeni’s “Roaring 2020s” scenario by potentially increasing profit margins, supporting real wage growth and personal consumption, tempering inflation, and potentially slowing the federal debt-to-GDP ratio increase.

The final point, in particular, helps explain why Nobel laureate economist and New York Times columnist Paul Krugman once said, “Productivity isn’t everything, but, in the long run, it is almost everything.” Yeah, it is.

The post Green Shoots of a 21st Century Productivity Boom appeared first on American Enterprise Institute – AEI.