An intriguing “what if” kind of economic question: What if no pandemic in 2020? Recall that 2019 was a pretty darn good year for the American economy. Unemployment was low (3.6 percent), economic growth was solid (2.5 percent), and productivity growth was robust (2.2 percent).

The productivity bit is particularly interesting given the zippy numbers we’ve seen in four of the past five quarters. I’ve certainly wondered if that recent good performance is merely a continuation of the 2019 upturn now that the economic chaos of the pandemic years recedes ever further in time.

If so, then perhaps we’ve seen the end of a 21st-century productivity slowdown that economists typically date as beginning in the mid-2000s, although you can fiddle with the exact start dates, such as if you want to incorporate the business cycle into your selection process. Anyway, the slowdown is well apparent in this data from the Federal Reserve Bank of New York, as presented in the recent blog post “The Mysterious Slowdown in U.S. Manufacturing Productivity” by economists Danial Lashkari and Jeremy Pearce:

Lashkari and Pearce specifically focus on manufacturing productivity, noting that the broader productivity slowdown

has been particularly stark in the manufacturing sector, which historically has been a leading sector in driving the productivity of the aggregate U.S. economy. … This fact is particularly puzzling in light of the widespread adoption of automation machinery and robots, which one might expect leads to a rise in labor productivity.

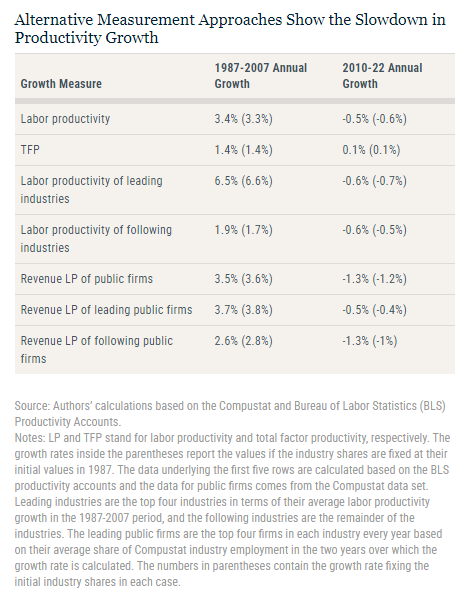

As seen in the above graphic, both the fastest- and slowest-growing industries (“leading” and “following,” respectively) are afflicted by the slowdown.

So what’s going on here? Lashkari and Pearce run through a number of possible culprits. For example: To determine if weaker capital investment is a cause, they examined total factor productivity (TFP), which measures productivity growth beyond what can be explained by changes in capital and labor inputs. If weak capital investment were the sole cause of the labor productivity slowdown, one would expect TFP — typically used as a measure of innovation — to continue growing. But their analysis of manufacturing TFP from 1987 to 2022 shows a significant decline, particularly after the Great Recession, with average annual TFP growth declining from 1.4 percent (1987-2007) to just 0.1 percent (2010-2022). This parallel decline in both labor productivity and TFP suggests capital investment isn’t the whole story.

Their conclusion isn’t satisfying, unfortunately:

The slowdown in labor productivity in manufacturing is one of the most important long-run issues in the United States that remains puzzling to economists and policymakers. This post points out that this development is common across industries and firms, with even the fastest-growing industries and the largest firms experiencing the slowdown. It is left to academics and policymakers to clear up the mystery about what factors are behind the ubiquitous slowdown in productivity.

This conclusive lack of a hard conclusion for this productivity mystery is one reason I recommend a multifaceted approach toward pro-productivity policy in my 2023 book, The Conservative Futurist: How To Create the Sci-Fi World We Were Promised, including tax, regulatory, public investment, and education policy.

The post The mystery of weak manufacturing productivity appeared first on American Enterprise Institute – AEI.