By James Pethokoukis

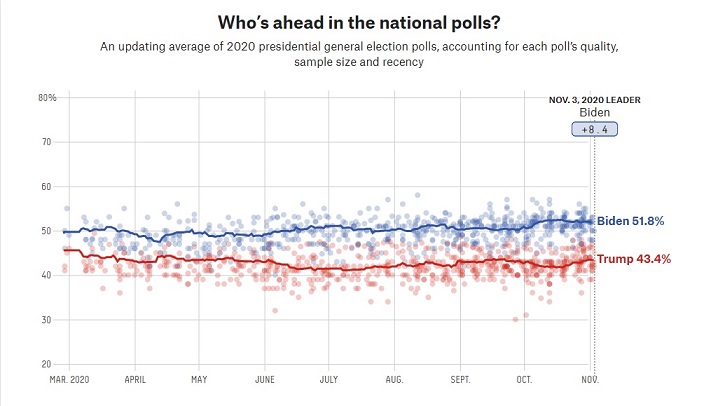

Public opinion polls in 2020 pointed toward an easy presidential election win by Joe Biden over Donald Trump. The FiveThirtyEight polling average had Biden winning by 8.4 percentage points (see chart below), and the RCP average had him up by 7.2 points. Biden actually won by a narrow 4.4 percentage points.

Betting markets were far more skeptical of a near-landslide by Biden. PredictIt, for instance, gave Biden a 61 percent chance of winning. The accuracy of forecast markets over polls can be better seen in the state-by-state results, as this post-election Fortune piece shows:

[Betting] odds forecasted that Biden would win the election with 310 electoral college votes, according to US-Bookies, despite some polls predicting a momentous landslide that would have given Biden as many as 350 electoral votes. With the winner now called in all 50 states, Biden will end up winning the White House with 306 electoral votes, just shy of betting markets’ 310-vote projection. Betting odds [also] appeared to provide a more realistic reflection of the dynamics in states like Florida, which Trump won handily despite many polls giving Biden an edge going into the election. While polls had Biden ahead by roughly 1% on average in Florida, according to RealClearPolitics, oddsmakers gave Trump 8-to-13 odds—or a 62% implied probability—of carrying the state, per US-Bookies. Likewise, in Texas, many polls indicated that Biden would be competitive in a state that Republicans have dominated for the last 40 years. But the odds gave Trump a 1-to-3 chance, or 75% probability, of winning Texas, which he eventually did by nearly 6 percentage points.

And what do betting markets say today about the 2022 midterms? PredictIt gives the GOP a 71 percent chance of taking control of Congress. That’s down 5 points from just before the US Supreme Court overturned Roe v. Wade. But to the extent that economic factors will prove more important than the Court’s decision, Republicans should be favored to win. Right now, it’s looking like the Inflation Election. Here’s a bit from new Goldman Sachs analysis looking at the relationship between economic variables and election results (bold by me):

Republicans look very likely to win a majority in the House of Representatives. The thin 5-seat majority Democrats now hold (counting vacant seats) is much smaller than the average midterm loss for the President’s party over the last 70 years of around 25 seats. The economic environment suggests larger-than-average losses. We revisit our prior work on the relationship between economic performance and election outcomes, adding inflation measures to the variables we normally consider. We find that headline CPI and gas prices are roughly equal in their statistical significance for midterm election results, but neither is as strong a predictor of election result as real disposable income growth, which has declined more over the last year than in any midterm election year since the data began.

What’s interesting here is that inflation by itself is not as important as its impact on real income. If nominal income were higher but inflation the same, real income would be higher and the environment would likely be better for Democrats. That’s what GS means by growth being more important than inflation.

One other point: Even though Election Day is still four months away, history suggests the economic picture is pretty much done cooking, at least as far as its electoral impact (bold by me):

Growth indicators are most important in Q2, while inflation matters early in the year. In regressions of the share of the popular vote that the President’s party wins in November on various monthly economic indicators, we find that growth-related indicators like real disposable income growth and change in payrolls are better predictors of the election outcome using values in April, May, and June. Inflation-related measures like headline CPI and gasoline prices have a stronger relationship using values early in the year, though we note that this relies on a relatively small sample of 18 midterm elections, many of which occurred during periods when inflation was not a major factor. Regardless, we think the main message this sends is that by mid-year, voters’ views regarding the economy are largely set and that policies to incrementally lower inflation ahead of the election, for example, might not have much of an effect on the outcome.

The post The Inflation Election: Economics Factors May Have Already Cooked the Midterm Election Results appeared first on American Enterprise Institute – AEI.